The SBA 7(a) Loan Program: Maximum Leverage for Florida Businesses

The SBA 7(a) Loan Program: Maximum Leverage for Florida Businesses

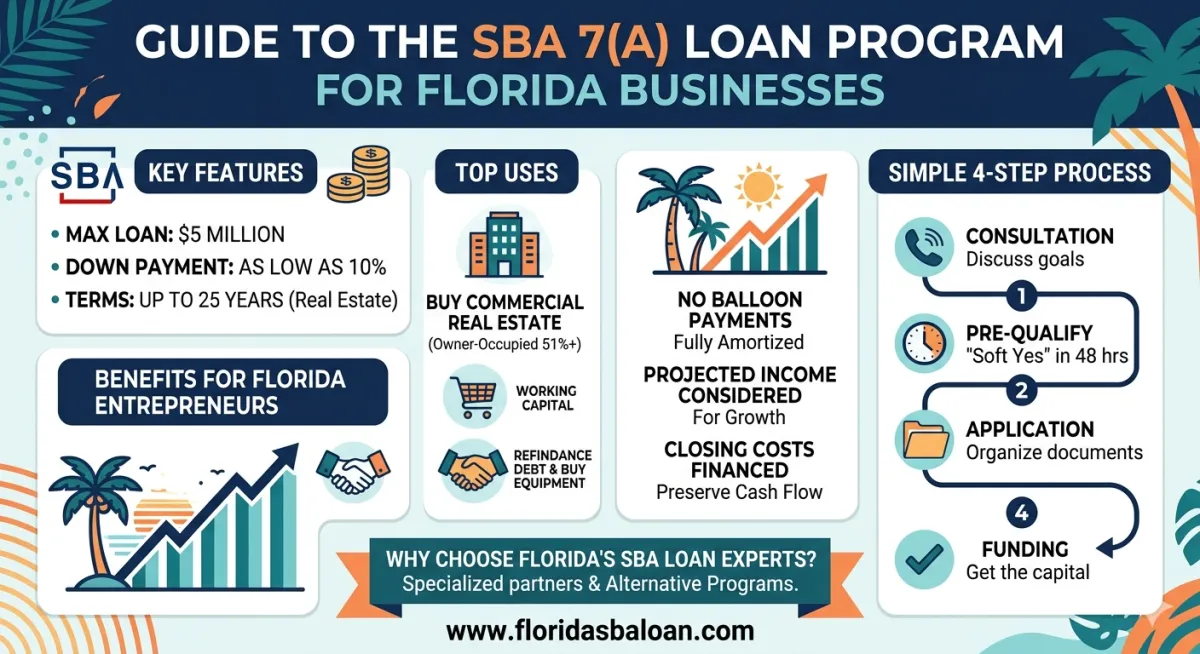

When it comes to purchasing your own building, acquiring equipment, or obtaining essential working capital, the SBA 7(a) loan program is widely considered the premier financing tool for Florida entrepreneurs. It offers a unique combination of maximum leverage and incredibly competitive rates that traditional conventional loans often cannot match.

SBA 7(a) loans are specifically designed to help small business owners purchase, construct, or improve commercial buildings, while also providing flexible capital for furniture, fixtures, equipment, and debt refinancing.

Advantages of an SBA 7(a) Loan

Higher Leverage: Access more capital than a conventional bank could offer from its own portfolio.

Lower Down Payments: Preserve your cash flow with equity injections as low as 10% for many projects.

Fully Amortized Terms: For real estate secured loans, enjoy terms up to 25 years with no balloon payments.

Government Guaranteed: Because the SBA guarantees a significant portion of the loan, lenders can provide higher Loan-to-Value (LTV) ratios.

Closing Cost Financing: Essential costs like appraisal fees, environmental reports, and contingency fees can often be rolled into the total financing.

Projected Income Consideration: Unlike conventional lending, our partners can consider projected income in addition to historical cash flows—an immense advantage for growing Florida businesses.

Structuring Your SBA 7(a) Loan

The SBA 7(a) program typically involves a partnership between the borrower and the lender:

Loan Amounts: Up to $5,000,000.

Borrower Contribution: A small business owner typically contributes a down payment of at least 10% of the total project cost. (Note: Startups or special-use properties may require slightly higher injections).

Lender Contribution: The lender provides a trust deed loan for up to 90% of the total project cost.

Flexible Rate Options: We offer various structures through our partners, including quarterly, 1-year, 3-year, and 5-year ARMs, as well as fixed-rate options.

Minimum Qualifications & Eligibility

To meet the core requirements for an SBA 7(a) loan in Florida, your business must:

Be organized as a for-profit entity (Sole Proprietorship, LLC, S-Corp, or C-Corp).

Owner-Occupancy: The business must occupy at least 51% of an existing building. For new construction, the business must occupy at least 60% of the property.

Economic Life: Any equipment financed into the project must have a remaining economic life of at least 10 years.

Collateral: While the SBA 7(a) program is flexible, additional collateral may be required where available to meet specific coverage ratios.

Why Choose Us for Your SBA 7(a) Financing?

Navigating federal loan programs requires a partner who understands both the local Florida market and the intricacies of SBA underwriting. We partner with elite investors and banks who specialize in the 7(a) program to ensure your application is positioned for success.

Ready to see if you qualify? Whether you are looking for a small-balance loan or a multi-million dollar real estate acquisition, our team is ready to provide a free initial assessment of your project.

Contact Us

Expert Tax and Accounting Services

Contact us today to learn how we can help you with your tax and accounting needs.

Our team of experts is dedicated to helping individuals and businesses achieve financial success.

Links

Terms of Use

Privacy Policy

Cookie Policy

© 2026. Commercial Loans Florida, Inc.. All rights reserved.